HOUSING

Mortgage Math

Not that you asked, but millions use this calculation without knowing why

With all of the news of people moving during the pandemic, low loan interest rates, and record housing prices, the estimate by the U.S. Census Bureau is that home ownership rates is down slightly year-over-year.

Mortgages are still a prevalent method for funding housing. From the Feds, outstanding mortgages have grown from nearly $6 trillion to over $16 trillion since 2020.

That is a lot of money, and a lot of people do not have a basic understanding of how the mortgage is calculated or how it works. Let’s take a look.

Mortgage Math

Googling mortgage calculator will yield more than 300 million results, and after a few ads this appears:

Very easy to use, and helpful for guidance on a monthly mortgage payment. There are many considerations in affording a home, but the mortgage cost tends to be the upfront number.

This is article is not covering the benefits of owning a home or renting, or a cost analysis of either.

Mortgage Costs

Home ownership costs are often thought of as PITI: Principal, Interest, Taxes, Insurance (home). There can be other costs: homeowner association dues, mortgage insurance, maintenance and repair, utilities, and more. This article is concentrated on Principal and Interest.

Staying with the example above, with just three inputs (Mortgage Amount, Interest Rate, and Mortgage Period) the monthly Payment is calculated. Breaking those down:

- Mortgage Amount is the dollar amount borrowed. There are other costs associated with buying a home — only the loan amount is covered in the mortgage calculation

- Interest Rate is expressed in an annual rate. The actual calculation for a mortgage payment uses a monthly rate, as interest is calculated each month. The monthly interest rate is the annual interest rate ÷ 12.

- Mortgage Period is expressed in years. The actual calculation for the mortgage payment uses number of payments, which is typically monthly. For a 30 year loan, that is 360 payments.

The mortgage cost is noted as $452,367, while the loan is $280,000. The difference is $172,367. That is the total cost of the interest on the loan.

The Calculation

Various sites and people use different variables in displaying the calculation. The loan amortization calculation comes down to:

P = L[i(1 + i)^n]/[(1 + i)^n — 1]

Payment = Loan [(interest rate * ( 1+ interest rate)^number of payments)] ÷ [(1+interest rate)^number of payments minus 1]

No need to memorize or understand that, unless you want to. There are plenty of on-line calculators, and if working with a mortgage provider, they will provide an amortization schedule. You can fact check their work using on-line calculators.

Here is a derivation proof written by Dr. Jennifer Golbeck, if you are interested in the math behind the calculation. And here is a YouTube by Mr. Mannion’s Math if you prefer video.

Other loans exist than a conventional loan, such as adjustable rate and interest-only. They use the same calculation at their base.

Why That Calculation

The history of the calculation might be lost. The history is not in The Mortgage Encyclopedia (non-affiliate link to Amazon). In checking with a property mortgage historian at the Federal Reserve, they had no knowledge of the amortization calculation in terms of where it was developed, by whom, et cetera.

Please let me know if you happen to know the history of the amortization calculation: who developed it, where, when, how easily was it adopted.

We do accept it as the calculation. If you ask a loan broker they will tell you it is the standard, but not why it is the standard. Perhaps they will point back to loan changes of the 1930s in the U.S., but the amortization calculation predates that into the 1800s in the U.S. and England (at minimum).

Calculating the Loan Payments

- Mortgage Amount (L) = $280,000

- Interest rate (i) = 3.5% monthly, or 0.2917% monthly

- Mortgage Period (n) = 30 years, which is 360 payments

The unknown is the payment per month (P), and that is what the calculation tells us.

Payment = Loan [(interest rate * ( 1+ interest rate)^number of payments)] ÷ [(1+interest rate)^number of payments minus 1]

Payment = [$280000(.0029167(1+.0029167)³⁶⁰)] ÷ [(1+.0029167)³⁶⁰ minus 1)] = $1257.33

Again, don’t memorize that!

The monthly Payment is $1257.33. In a conventional loan, where the interest rate does not change, that amount is due every month for the duration of the loan.

Easy Deconstruction of the Mortgage Payment

The monthly Payment is set at $1257.33, and it is broken into the Principal and the Interest. How much goes toward Principal, and how much toward Interest?

The Interest amount is calculated first each month. It is simply:

Outstanding Loan * Monthly Interest rate

Reminder: Monthly Interest is the annual rate ÷ 12

For the first month of the loan:

Interest = $280,000 * .0029167 = $816.67

The Principal is the monthly Payment minus the Interest paid

Principal = $1257.33 minus $816.67 = $440.66

That’s it.

The second monthly payment is calculated using the new amount of Principal remaining.

$280,000 minus $440.066 = $279,559.34 remaining

Interest = $279,559.34 * .0029167 = $815.38

Principal = $1257.33 minus $815.38 = $441.95

And so forth…

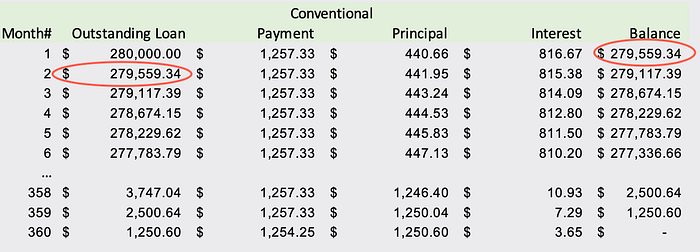

Amortization / Loan Schedule

Online calculators and loan officers can provide a loan amortization schedule detailing every month of the loan. It breaks out the monthly payment into how much is Principal and how much is Interest. It looks akin to this:

The loan balance decreases by the Principal amount each month, and that new Principal amount is used to determine the new Interest paid.

Wrap-up

Home ownership is essentially flat over the last year, while the amount held in mortgages is nearly tripled in the last 20 years. Those mortgages go through the same formula for repayment (not that we know why!).

Understanding the math is about awareness.

- You can see why interest is so front-loaded in the Payments

- You can see why the Principal is chipped away so slowly to begin with

Without modifying the loan (such as a refinance), the Payment per month is set in a conventional loan. You can accelerate the loan repayment by paying more Principal each month, as reviewed here:

This article is for informational purposes only, it should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.